Operating Income Formula | Overview | Example

Operating Income Formula: Operating income, often referred to as EBIT or earnings before interest and taxes, is a profitability formula that calculates a company’s profits derived from operations.

In other words, it measures the amount of money a company makes from its core business activities not including other income expenses not directly related to the core activities of the business.

Net Operating Income Formula

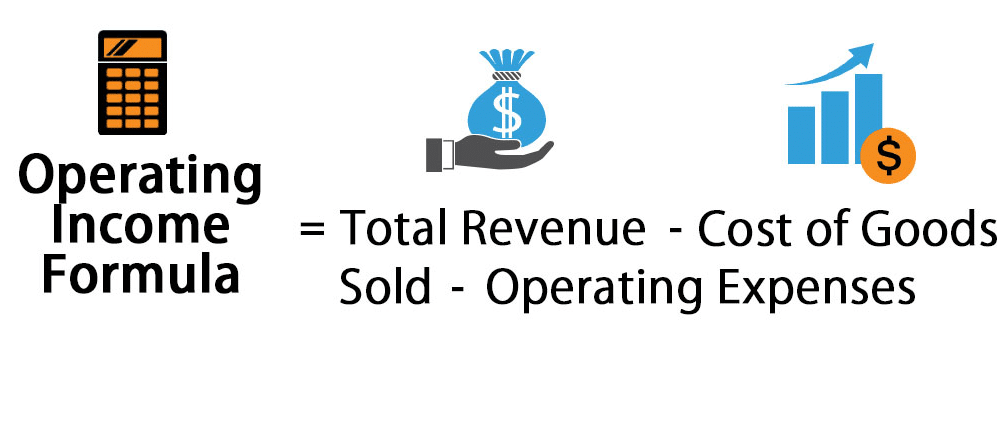

Operating Income = Revenue – Cost of Goods Sold (COGS), Labor, and other day-to-day expenses

Operating income is also called Earnings Before Interest and Taxes (EBIT).

It is important to understand what expenses are included and excluded when calculating operating income. It typically excludes interest expense, nonrecurring items (such as accounting adjustments, legal judgments, or one-time transactions), and other income statement items not directly related to a company’s core business operations.

Net Operating Income Formula Managerial Accounting

Investors, creditors, and company management use this measurement to evaluate the efficiency, profitability, and overall health of a company. Remember, the operating income definition states that it measures the profits from the core business activities without taking into account extraordinary items. The higher the operating income, the more likely the company will be profitable and able to pay off its debt.

Investors and creditors also follow this number very closely because it gives them an idea of the future scalability of the company. For instance, a positive trending operating profit can indicate that there is more room for the company to grow in the industry. A sinking number indicates the opposite.

Management is well aware of this fact and can try to fraudulently change the ratio by accelerating revenue recognition or delaying the recognition of expenses. Both of these tactics are against GAAP.

How Do You Calculate Operating Income?

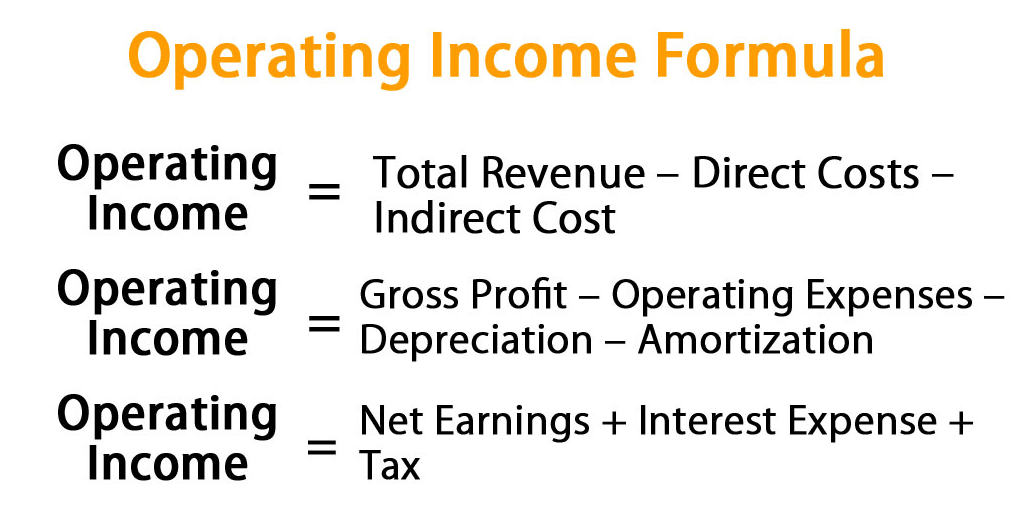

- Operating income = Total Revenue – Direct Costs – Indirect Costs. OR.

- Operating income = Gross Profit – Operating Expenses – Depreciation – Amortization. OR.

- Operating income = Net Earnings + Interest Expense + Taxes. Sample Calculation.

What Is Included In Operating Income?

How Do You Calculate Operating Income Ratio?

What is EBIT Formula?

Target Operating Income Formula

A multi-step income statement lists this calculation at the end of the operating section as income from operations. This section always is presented before the non-operating and income tax sections to compute net income.

This is an important concept because it gives investors and creditors an idea of how well the core business activities are doing. It separates the operating and non-operating revenues and expenses to give external users a clear picture of how the company makes money.

Keep in mind that just because a business shows a profit on the bottom line for the year doesn’t mean the business is healthy. It could actually mean the opposite. For instance, a business might be losing customers and downsizing. As a result, they are liquidating their equipment and realizing huge gains. The core activities are losing money, but equipment sales are making money. This business is clearly not healthy.

Net Operating Income Formula Accounting

Operating income, or EBIT, is important because it is an indirect measure of efficiency. The higher the operating income, the more profitable a company’s core business is.

Several things can affect operating income (such as pricing strategy, prices for raw materials, or labor costs), but because these items directly relate to the day-to-day decisions managers make, operating income is also a measure of managerial flexibility and competency, particularly during rough economic times.

Operating income provides investment analysts with useful information for evaluating a company’s operating performance without regard to interest expenses or tax rates, two variables that may be unique from company to company, and enables one to analyze operating profitability as a singular measure of performance. Such analysis is particularly important when comparing similar companies across a single industry where those companies may have varying capital structures or tax environments.

Formula For Operating Income

Operating Income = Revenue – Cost of Goods Sold (COGS), Labor, and other day-to-day expenses

Operating expenses typically include all of the costs associated with running the core business activities. Here are a few examples:

- Rent

- Utilities

- Insurance

- Wages

- Commissions

- Freight and Postage

- Supplies expense

Depreciation and amortization are often included in this list and always used in the operating income equation. Let’s take a look at an example.